We Need to Get Creative to Save Social Security

With insolvency just 6 years away, only a new approach can save FDR’s vision of an earned benefit that keeps older Americans out of poverty.

Ever since Franklin Roosevelt created Social Security in 1935, it has rested on the principle that Americans should earn their retirement benefits. The president was a deep believer in the moral importance of work, who also knew his plan would be more politically durable if voters felt as if they had personally paid into it. So the program was designed to mimic a traditional pension, where payroll taxes represented a worker’s contributions and benefits increased for higher earners.

Nearly a century later, the social compact behind Social Security is fraying. Americans have not paid nearly enough into the program to cover the benefits they’ve been promised. As a result, its primary trust fund is now officially projected to run out of money in 2032. If policymakers fail to act in the next president’s term, beneficiaries will face an automatic 22% cut in order to keep payouts in line with contributions.

Policymakers could have saved the system as we know it with modest tweaks had they acted earlier. For example, today’s retirees could have paid slightly higher tax rates over their working lives to adequately fund their benefits. But instead, they elected lawmakers who either ignored the problem or actively made it worse.

Now, it’s effectively too late to prevent massive cuts without abandoning the notion that today’s Social Security beneficiaries actually paid for their benefits. Every dollar that must be raised from higher taxes on today’s workers to prevent a cut for current retirees is a wealth transfer from young to old — from a generation that inherited this shortfall to the one that let it grow.

But policymakers can uphold FDR’s vision of a program in which benefits are earned through work without binding themselves to the false pretense that seniors paid for their benefits. It just requires them to redefine the mechanism by which benefits are earned.

To show them how, my team at the Progressive Policy Institute (PPI) developed a package of reforms built around an innovative new concept: Instead of calculating benefits based on how much income a person earns throughout their career, Social Security would award benefits based on how many years someone works. In other words, a riveter who earns $60,000 annually and a lawyer who earns $300,000 would get the same monthly check in retirement as long as they put in the same number of years on the job.

This redesign would strengthen Social Security’s finances by reducing the outsized benefits that go to high-earners. It would also increase support for seniors with the greatest financial need: under our plan, anyone who works for at least 20 years would receive a benefit large enough to keep them out of poverty, which isn’t guaranteed under today’s system. And it would protect older Americans by preventing automatic benefit cuts slated to take effect in just six years — all without drastically higher taxes on today’s workers.

Importantly, this reform would reinforce Social Security’s premise as a benefit people earn rather than transforming it into a stereotypical redistributive welfare program, affirming the basic Rooseveltian vision.

Our proposal is not without its critics, however. Wendell Primus —– a longtime aide to former Speaker Nancy Pelosi —– and three of his colleagues at Brookings earlier this year published a critique titled “Insufficient financing should not provoke dramatic changes to Social Security.” Notably, the authors did not object to the specific merits of PPI’s proposal. Instead, they argued that policymakers should reject any plan that weakens the link between an individual’s Social Security benefits and their tax contributions into the program. In short, they want to maintain the popular fiction that Social Security works sort of like a normal retirement account.

I don’t want to get into an endless debate over the merits of every specific detail of each proposal, because those will almost certainly be iterated upon between now and when Congress ultimately comes around to seriously considering solutions. But exploring the fundamental weaknesses of their criticism and the alternatives they propose actually shows the impracticality of clinging to the thin pretense that seniors have paid for their benefits — namely, that tying benefits to income necessitates showering benefits on rich seniors who don’t need them or cutting benefits for poor seniors who actually depend on them. It’d be better for policymakers to unshackle themselves from the failing approach of yesteryear and embrace some unconventional ideas.

Nobody Really Has a Plan to Save Social Security “As We Know It”

To demonstrate that Social Security can be salvaged without what he calls “radical changes,” Primus points to two alternative proposals: one he developed at Brookings, and one developed by the Bipartisan Policy Center’s Commission on Retirement Security and Personal Savings in 2016.

Let’s start with the BPC plan. I am intimately familiar with its strengths and weaknesses, perhaps more than almost anyone else, because I helped write it as the staffer specializing in Social Security on that commission.

The BPC plan was an attempt to adhere as closely as possible to the original design and goals of Social Security. To the extent policymakers are rigidly committed to that approach, I believe the BPC blueprint remains the best starting point for them. But even it struggles to achieve those aims.

The BPC plan would seek to fix Social Security’s financial trouble in part by raising the cap on how much of an individual’s income is subject to payroll taxes, which currently sits at $184,000. In return, higher earners would also receive some extra benefits when they retire — but they’d be extremely modest. The highest earners would receive just $1 in monthly benefits for every additional $20 of wages subject to new annual taxes, compared to a minimum of $3 under the current formula. At the same time, BPC’s plan would increase benefits for low earners more than it would increase their taxes.

The end result is a much, much flatter benefit structure than exists today. If the BPC formula were fully in place now, someone with $300,000 of average lifetime earnings would receive a monthly benefit just 50% more than someone who earned $60,000 despite having paid 400% more in payroll taxes.1 Although the link between contributions and benefits would technically remain, it would exist more in principle than in practice.

Even then, it is an incomplete solution to Social Security’s financial troubles. Had the BPC plan been enacted when we first proposed it, the program would have been made sustainably solvent. But enacting the plan today wouldn’t be enough to close the shortfall. Moreover, the burden of these reforms would fall more heavily onto younger Americans if the reforms began phasing in now, because people retiring over the past decade will have avoided most of the package’s benefit reforms as well as taxes on their final years of earnings. Both these problems will only grow worse the longer policymakers wait to act — further straining the link between contributions and benefits.

We Shouldn’t Give Even Bigger Benefits to Wealthy Seniors

Primus’s proposal also flattens benefits relative to contributions, although not quite as much as BPC’s does (the $300,000-earner would get monthly benefits approximately twice those of the $60,000-earner in his formulation, while paying five times as much in payroll taxes). But to adhere more closely to the principle that benefits reflect past contributions, Primus’s proposal would increase high-earners’ Social Security benefits relative to current law, in conjunction with their taxes. Ultimately, a future beneficiary who consistently earned more than $300,000 annually in today’s dollars would get benefits roughly 20% greater than they would under the current formula.2

It’s worth stopping here to point out that Social Security was not created to lavish wealthy seniors with large pensions. When the Social Security Act was passed, nearly half of older Americans lived in poverty. Even previously well-off seniors were left destitute by the Great Depression and in worse shape than working-age Americans. That problem was what a wage-replacement style retirement program needed to solve. FDR was clear about his intention: While signing the Social Security Act, he called it “a law which will give some measure of protection to the average citizen and to his family against … poverty-ridden old age.”

Thanks in large part to Social Security, today’s seniors are in much better shape relative to workers. In Primus’s estimation, just 6% of older Americans are in poverty — that’s lower than the poverty rate for Americans overall. Sixty-three percent of America’s wealth is owned by Baby Boomers and earlier generations. The top 10% of senior households have net worths exceeding $2.5 million. And the ratio of a senior’s income to a worker’s income is higher in the United States than in social democratic states like Sweden and Denmark.

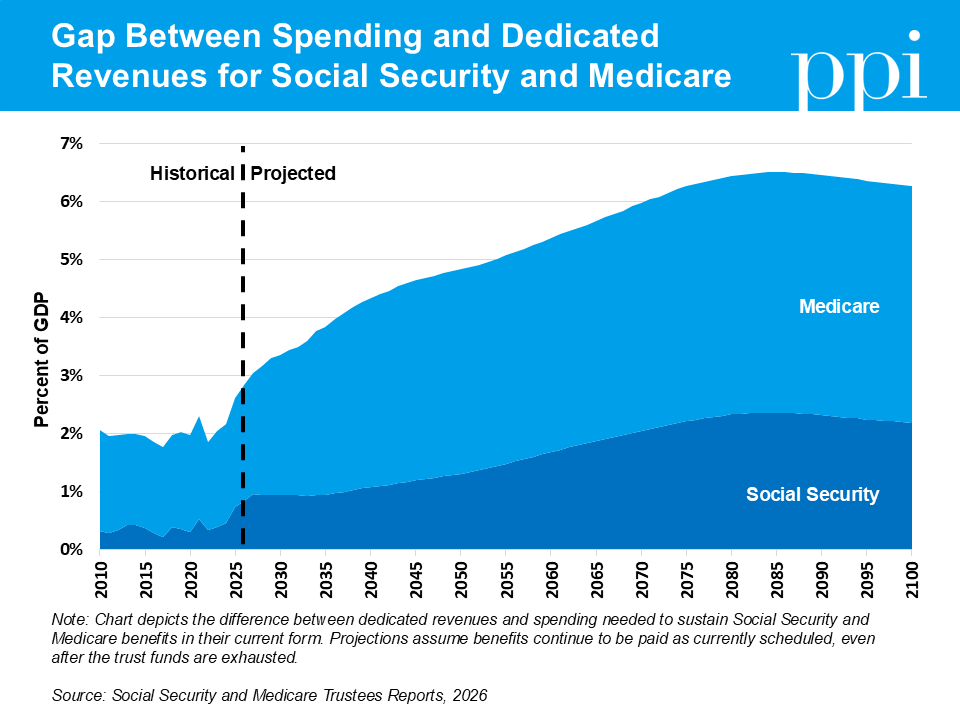

Yet working Americans are paying a much bigger price tag to support today’s retirees, despite now being positioned worse relative to them. For Social Security’s first 20 years, the program cost less than 2% of GDP. Social Security now costs more than 5% of GDP, and is projected to hit 6% of GDP by 2050. In the context of America’s growing budget deficits and many national needs, it makes little sense to continue paying massive benefits to high-income retirees who do not need them — let alone pay them even more.

Social Security Reforms Have to Fit Within the Broader Budget

One of the biggest problems with Primus’s plan is that it ignores the broader fiscal challenge facing the federal government. Yes, it would technically make Social Security solvent for the foreseeable future. But to do so, it depends on diverting taxes currently going to a Medicare trust fund into Social Security. So how would Primus plug that revenue gap? He doesn’t say — which is particularly ironic given that he complains that other plans “do not include any specific solutions for revenue changes.”3 This approach is especially problematic considering that the gap between spending and dedicated revenue for Medicare is growing much faster than it is for Social Security. And Primus has proposed costly benefit expansions that would make the gap even bigger, paid for by unspecified tax increases.

Primus’s approach demonstrates the dangers of trying to solve Social Security’s problems without taking into consideration the rest of the federal budget. When one looks at Social Security in isolation, even simplistic solutions like just eliminating the payroll tax cap make a lot of sense — why shouldn’t the richest of the rich pay at least the same rate as everyone else?

The problem is that scrapping the payroll tax cap is effectively a 12.4 percentage-point increase in the top marginal income tax rate. Combined with ordinary income taxes at the federal and state level, taxes at the top would approach the revenue-maximizing rate, making it difficult to raise taxes on the rich to pay for anything else. Yet when Social Security hits its cliff in 2032, the total federal budget deficit projected by the Congressional Budget Office will be roughly five times the size of Social Security’s annual deficit. If Congress has completely tapped out the reservoir of politically palatable tax hikes on the rich, where will they get revenue to pay for the bigger deficits facing other federal programs?

Unlike Primus, PPI developed and proposed our Social Security reforms as part of a comprehensive budget blueprint. Although PPI left open the question of which revenue source policymakers earmark for which spending program as a matter of accounting, we made sure the totality of our specified tax and spending changes would put the federal budget on a path to eventual balance (as did BPC in their most-recent budget plan).

To be sure, one need not solve the entirety of our nation’s fiscal problems to fix Social Security’s. But at the very least, it is essential for any plan that claims to shore up Social Security to work within a broader budgetary context instead of creating new problems.

Unconventional Reforms Can Help Social Security Better Fulfill its Mission

If even the most-balanced attempts to preserve the current system strain the link between contributions and benefits beyond reason, shower benefits on wealthy retirees who don’t need them, and/or worsen structural deficits in other programs, it’s time to ask ourselves: Does it really make sense for policymakers to bind themselves to it?

When it came time for me to re-evaluate Social Security in the context of PPI’s budget plan, I concluded the answer was no. My team believed we should develop a new offering — one that maintains the popular premise of Social Security as an “earned benefit,” but without having to give the biggest benefits to the people who need them least.

Our approach also unlocks additional benefits beyond reigning in Social Security’s deficits and refocusing the program on its original purpose of keeping older Americans from falling into poverty.

One upside to ditching the convoluted link between earnings and benefits is that it would make benefits more predictable and more reliable. To determine an individual’s benefit under the current system, they have to know exactly how much they earned every single year of their career and adjust it using formulas for wage growth in the time between the year of their earnings and when they become eligible for benefits. Furthermore, the specter of automatic benefit cuts makes it impossible to consider the benefit determined by the formula reliable.

By contrast, PPI’s proposal is simple for the vast majority of workers: add up the number of years they earned a credit for working, multiply it by the monthly benefit per credit, and boom — that’s their benefit. Because it has no shortfall, our proposal gives certainty that the current system cannot.

Another upside of our approach is that it allows policymakers to consider better alternatives to the current payroll tax. As it exists today, the payroll tax is regressive, imposing higher rates on people whose earnings fall below the cap than on those whose earnings fall above. Even the progressivity of federal income taxes does not totally offset this: someone who earns $200,000 pays a lower marginal tax rate than someone who earns half as much. That revenue structure may be a necessity if policymakers want to maintain the pretense that benefits are linked to contributions, but it is far from the most equitable or efficient tax policy.

Reform Plans Have More Common Ground Than They Appear

Despite the limits of their approach, I believe Primus and his colleagues at Brookings should be commended for trying to offer a constructive solution to the rapidly approaching Social Security crisis.

There is actually a lot of common ground among the Primus, BPC, and PPI proposals. All three propose to raise enough revenue to close at least half of the solvency gap. They all raise a disproportionate share of this revenue from higher-income Americans, who can afford to pay the most. And unlike those of some delusional politicians, all three plans recognize that some additional revenue will need to come from Americans across the income spectrum.

On the benefits side, all three plans propose to preserve or increase benefits for Americans most vulnerable in retirement. They propose to reduce the benefits of higher earners, at least as a proportion of the taxes they pay into the system (and thus flatten the benefit structure). And they aim to uphold the principle that Social Security should remain a benefit people can credibly claim they earn through work.

The big difference is whether we seek to give people greater benefits in retirement simply because they earned more when they were working, in an effort to maintain the fiction that Social Security beneficiaries paid for their benefits. Primus’s insistence that we do forces him to adopt policies that lead to undesirable outcomes, such as increasing benefits paid to the highest earners who need them least, paid for by a higher tax burden on future workers. Even though, as I argued earlier, it doesn’t really succeed in meaningfully keeping the link.

By contrast, PPI’s willingness to abandon the fiction allows us to refocus on optimal policy — what will lead to the greatest welfare for workers and retirees alike, while imposing the minimum intergenerational wealth transfer necessary. At the same time, we have found a way to preserve the earned nature of benefits. We acknowledge a fundamental truth: Today’s Social Security beneficiaries did earn their benefits through a lifetime of hard work. But they did not pay for their benefits. Let’s pursue a solution that reckons with this reality and better fulfills the promise of Social Security for everyone.

This is an illustrative oversimplification that doesn’t take into account formula phase-ins, indexation of previous years’ earnings to subsequent wage growth, and interactions with other provisions.

Technically, Primus would increase the highest-earner’s benefit by nearly 50% but then claw part of that back with an increase in the “normal” retirement age. Because this age is an arbitrary point between the minimum and maximum benefits age, which remains unchanged by the Primus plan, it is functionally no different than a proportionate benefit cut for high earners. It really just further underscores the convoluted hoops one must jump through when trying to uphold a link between earnings and benefits while minimizing regressive outcomes.

Primus offers a proposal for replacing the money his Social Security plan would take from Medicare’s Hospital Insurance trust fund, but a majority of the revenue comes from reallocating current-law general revenues. This just moves the gap from one part of Medicare to the other, which relies on significant general-revenue financing to pay benefits as-is.

| A guest post by

|

Or just raise the minimum wage to $30 and peg it to inflation (similar to the cost-of-living adjustment/COLA for SSA benefits) AND reduce the full-time workweek (overtime threshold) to 30 hours (and consider pegging it to productivity growth) while increasing the penalty to double time, which creates labor scarcity and strengthens worker's bargaining power.

Both these measures reduce income inequality, keep it down through automatic adjustments from the peg, and drive more income under the SSA taxable income cap, plugging most of the projected benefits shortfall. (Not to mention reduce demands on the social safety net part of the budget - SNAP, TANF, Medicaid, etc.)

No new law and restructuring needed. And no, I already don't want to retire at 67 and this proposal raises the retirement age some more. The AI robots are supposed to be coming to take all the jobs of workers that are supposedly too few to support retiree benefits (make that make sense!), so seems to me we should be lowering the retirement age.

P.S. As for Medicare, they pay health care bills; they don't set prices. Fixing their bloated budget amounts to fixing the exorbitant cost of drugs, medical equipment, health care professionals (especially physicians and surgeons), and privatized Medicare (aka Medicare Advantage). In fact, allowing Medicare to cover everyone (the public option) and giving it full monopsony power to bargain would go a long way towards reducing costs, only needing a modest increase in the tax. Again, nothing complicated here, except entrenched, well-financed political and economic special interests.